The concept of holding and subsidiary companies plays a significant role in shaping modern corporate structures in Nepal. Rather than operating as independent entities, many businesses today function as part of interconnected corporate groups designed to improve efficiency, manage risk, and expand strategically. Chapter 13 of the Companies Act 2063 lays the foundation for these relationships by defining control mechanisms, documentation requirements, and restrictions to ensure transparency and good governance.

This framework is crucial for directors, shareholders, investors, and corporate professionals seeking to understand how group companies function within Nepal’s regulatory environment. It emphasises both corporate flexibility and accountability, ensuring that companies operate efficiently while maintaining the integrity of their financial and operational reporting.

Definition and Nature of Holding and Subsidiary Companies

Holding Company

In accordance with the Companies Act 2063, Section 2(d), a holding company is a company that controls one or more subsidiary companies.

The defining feature of a holding company is its ability to control decision-making within its subsidiaries, either through share ownership or influence over the subsidiaries’ boards of directors.

Essentially, the holding company stands at the top of the corporate hierarchy, guiding the overall strategy and governance of its subsidiaries while still recognising their separate legal identities.

Subsidiary Company

According to the Companies Act 2063, Section 2(e) clearly defines a subsidiary company as one controlled by a holding company.

Although it operates independently and maintains its own rights and obligations under the law, the subsidiary functions under the direction or oversight of the holding company.

This relationship enables coordinated operations while maintaining distinct legal and financial accountability.

Establishing Control Over a Subsidiary Company

Section 142 of the Companies Act, 2063 defines how a holding company can establish control over a subsidiary through two main methods:

- Control Overboard Formation - A holding company may directly or indirectly influence the appointment of directors on the subsidiary’s board, allowing it to control strategic and operational decisions. This control can also be exercised through intermediaries or other subsidiaries, forming multi-tiered corporate structures.

- Majority Share Ownership - When a holding company owns more than 50% of the voting shares in another company, it gains the power to appoint directors and make key corporate decisions, effectively controlling the subsidiary.

The Act also recognises multi-tiered structures, where control extends through layers of subsidiaries.

For instance, if Company A controls Company B, and Company B controls Company C, then Company A also controls Company C.

Additionally, Section 142(3) includes deemed control through nominees or agents, ensuring that control cannot be concealed through intermediaries.

However, the Act excludes cases where shares are held merely to protect debenture rights or used as loan security, ensuring that only genuine, intentional control qualifies under the holding-subsidiary relationship.

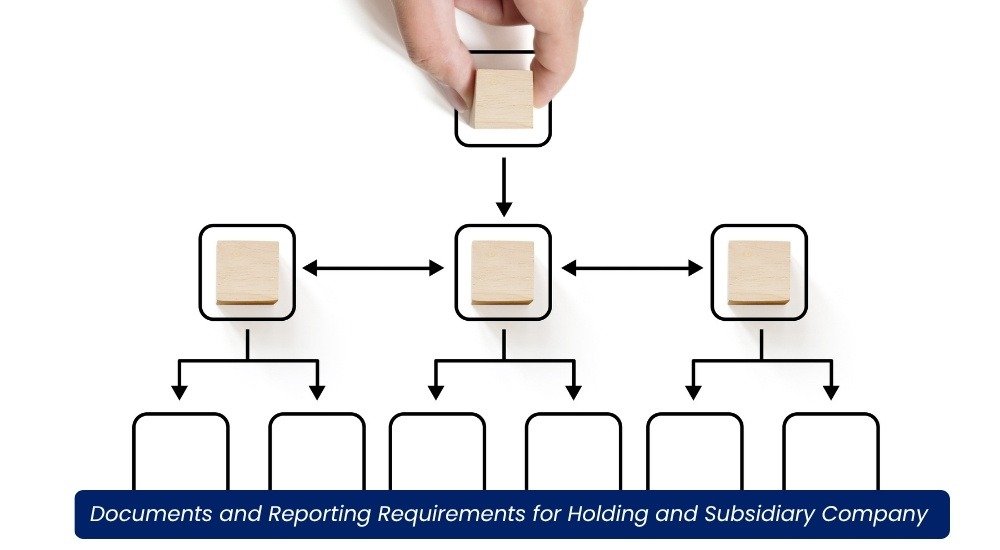

Documents and Reporting Requirements

Section 143 of the Companies Act sets out extensive reporting and disclosure requirements for holding companies.

These provisions ensure transparency across the entire corporate group, providing shareholders with a clear understanding of the subsidiary’s financial and operational performance.

A holding company must attach the annual financial statements of each subsidiary to its own balance sheet.

This includes the subsidiary’s balance sheet, income statement, and other relevant accounts for the previous budget year.

The purpose is to provide company shareholders with a complete view of the group’s performance, not just that of the parent company.

Along with the financial statements, the subsidiary’s board report must also be included.

This report provides a management perspective on performance, strategy, and the subsidiary’s challenges during the budget year.

The auditor’s report on the subsidiary company must also be enclosed.

This ensures that the financial data presented is verified and credible, enhancing confidence in the overall group’s financial transparency.

The holding company must disclose full details of its investment in each subsidiary as of the end of the budget year.

This includes the value of shares held and the percentage of ownership, allowing stakeholders to understand the extent of the holding company’s financial involvement.

When the budget years of the holding and subsidiary companies differ, the holding company must disclose any changes in control, rights, or interests that occurred during different periods.

This ensures that significant developments are not overlooked due to differing reporting timelines.

Prohibition on Subsidiary Investment in Holding Company

Section 144 prohibits a subsidiary company from investing in its own holding company. This restriction is crucial for maintaining the integrity of financial reporting and preventing circular ownership structures that could distort financial statements.

Allowing such investments could lead to inflated share capital or artificial control arrangements, undermining shareholder interests.

The prohibition ensures that subsidiaries’ funds are not misused to support the holding company’s capital or management control, protecting minority shareholders and promoting sound governance.

Practical Implications for Corporate Governance

The framework established by Chapter 13 has significant implications for corporate governance in Nepal:

The documentation and disclosure obligations under Section 143 promote financial transparency across corporate groups.

Shareholders and investors gain insight into subsidiary performance, enabling better oversight and decision-making.

Directors of holding companies must ensure the timely and accurate collection of information from subsidiaries to meet reporting requirements.

Non-compliance can result in regulatory penalties and potential personal liability for directors and officers.

The Act safeguards the interests of shareholders, creditors, and regulators by preventing misuse of power and ensuring full disclosure of subsidiary operations.

These measures enhance investor confidence and contribute to a healthier business environment.

Nepal’s Approach in an International Context

Nepal’s legal framework for holding and subsidiary companies, while mirroring international corporate law principles, incorporates unique elements to address local business realities.

Nepal’s legal framework, with its emphasis on transparency, disclosure, and control definitions, aligns seamlessly with global governance standards. This alignment not only promotes investor confidence but also provides a reassuring backdrop for foreign investment in the country.

By accommodating multi-tiered subsidiary structures and introducing anti-avoidance provisions, Nepal’s Companies Act ensures that even complex group structures are under the vigilant eye of regulatory supervision. This proactive measure prevents potential misuse of such structures, providing a sense of security to all stakeholders.

Conclusion

Chapter 13 of the Companies Act, 2063, provides a detailed and robust legal structure for holding and subsidiary company relationships in Nepal.

It clearly defines control mechanisms, enforces comprehensive disclosure requirements, and prohibits practices like circular ownership that could compromise transparency.

These provisions strengthen corporate governance, enhance shareholder protection, and promote accountability across group companies.

As Nepal’s corporate sector grows and becomes more complex, the principles outlined in this chapter will remain vital for maintaining integrity, transparency, and investor trust within the corporate ecosystem.

For businesses and professionals operating within corporate groups, understanding and adhering to these legal provisions is not just a compliance requirement.

It is a cornerstone of sustainable and responsible business practice in Nepal, underscoring the necessity of ethical conduct in the corporate sector.